What Is Lean Accounting?

Lean Accounting is the application of lean thinking to all accounting and finance processes and systems and is an essential component of a successful lean transformation for any organization.

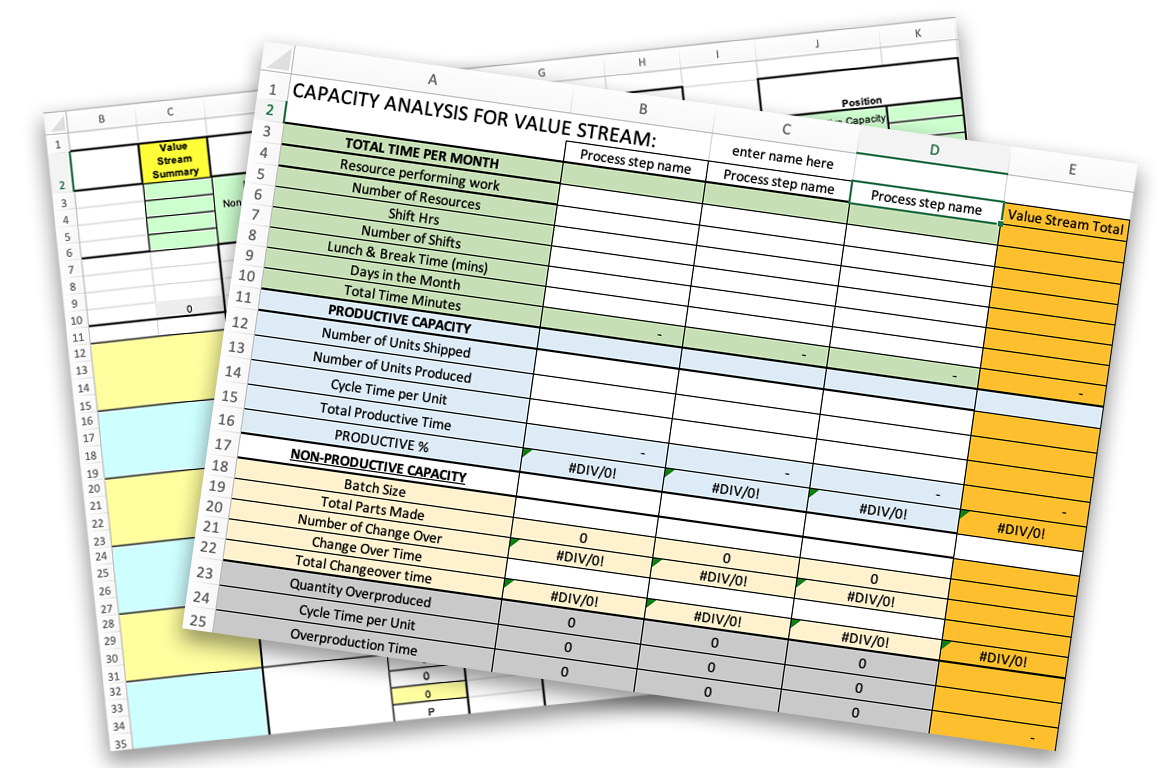

Lean Accounting Certification Program

BMA’s online, self-paced certification courses are designed to demonstrate individual competency and knowledge in understanding the principles, practices and tools of a lean accounting system. You will validate your knowledge by taking quizzes at the end of each class. These certification courses are based on BMA’s proven approach to implementing lean accounting in all types of companies in any industry.

Learn More